Markets

-

Angolan diamonds: into the XXI century

If you’re interested in (exploring for and mining) diamonds in Angola (or elsewhere), I and José Abranches will…

-

BHP to invest US$400m to address climate change

CEO Andrew Mackenzie has announced a range of new measures aimed at evolving BHP’s response to climate change.

-

SME Guide For Reporting Exploration Information, Mineral Resources and Mineral Reserves

The 2017 SME Guide for Reporting Exploration Results, Mineral Resources, and Mineral Reserves has been adopted by the…

-

Transition into a new mobility: US National Academies perspectives

The trend towards electrification, especially in mobility, is a major priority in the European Union. Electrical networks’ management,…

-

2017 diamond flows and what lies ahead

IDEX just reported on the 2017 Diamond Pipeline in the latest number of their online magazine. The 2017…

-

gold, gold, gold, crypto coins, blockchain and diamonds

What happened, what may happen For those interested in the yellow metal, the World Gold Council recently released…

-

Nova Edição do Curso sobre Avaliação de Jazigos e outros Activos Minerais

IST (FUNDEC – 21, 22 e 23 de Junho 2017) – Luís Chambel (Sínese) e Jorge de Sousa (IST)…

-

ANNUAL Antwerp World Diamond Centre 2016 REPORT

AWDC (Antwerp World Diamond Centre) Annual 2016 Report is now available online Available for download via this link. Always…

-

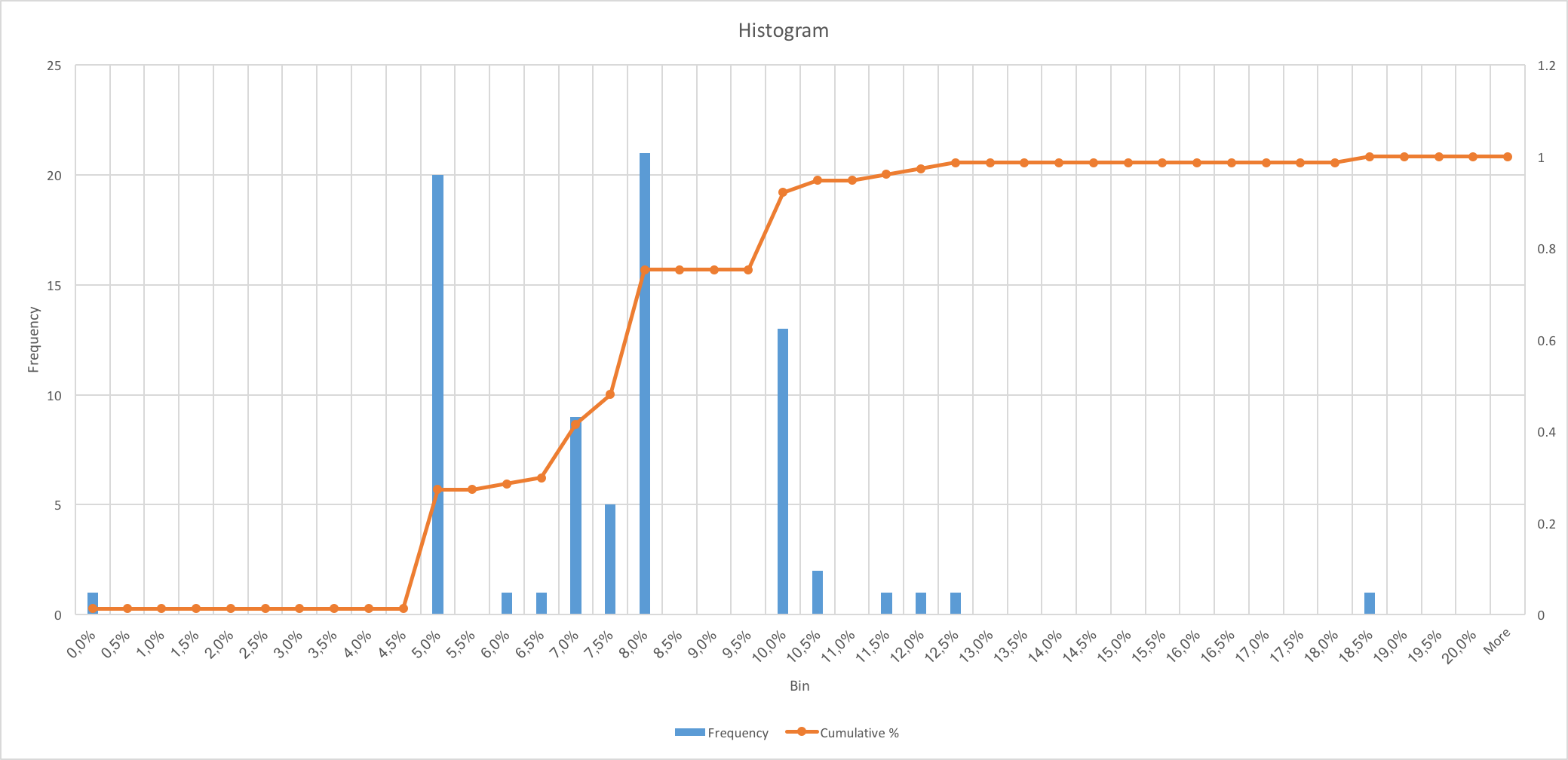

wrong, something is very wrong

RISK UNDERVALUATION IN MINERAL PROJECTS Reporting to markets should (have to!) be complete, independent and competent. Risk is…

Tyler Moore

Hello, my name is Tyler Moore and with the help of many people I made this template. I made it so it is super easy to update and so that it flows perfectly with my tutorials. I wish you the best of luck with your business, enjoy the adventure.

Must Read

Categories

- Africa

- Ambiente

- Andaraí

- Angola

- Brasil

- Canadá

- Chronicles

- Cobre

- Congo – Brazzavile

- Cortiça – Cork

- Data Analysis

- Diamantes

- Diamantina

- Diamonds

- EconGeo

- Economic Geology

- ESG

- Estados Unidos

- Gems – Gemas

- Gold

- Judo

- Markets

- mining

- Moçambique

- Mozambique

- Namibia

- NatStone & other NatMaterials

- Ordem dos Engenheiros

- Portugal

- reports

- Rochas e Minerais

- Rocks

- rubi

- Sinese

- Sri Lanka

- Sri Lanka

- Stone – Pedra

- Sustentabilidade

- Travel

- Uncategorized

- Vida portuguesa – Life in the West Coast

- zinco